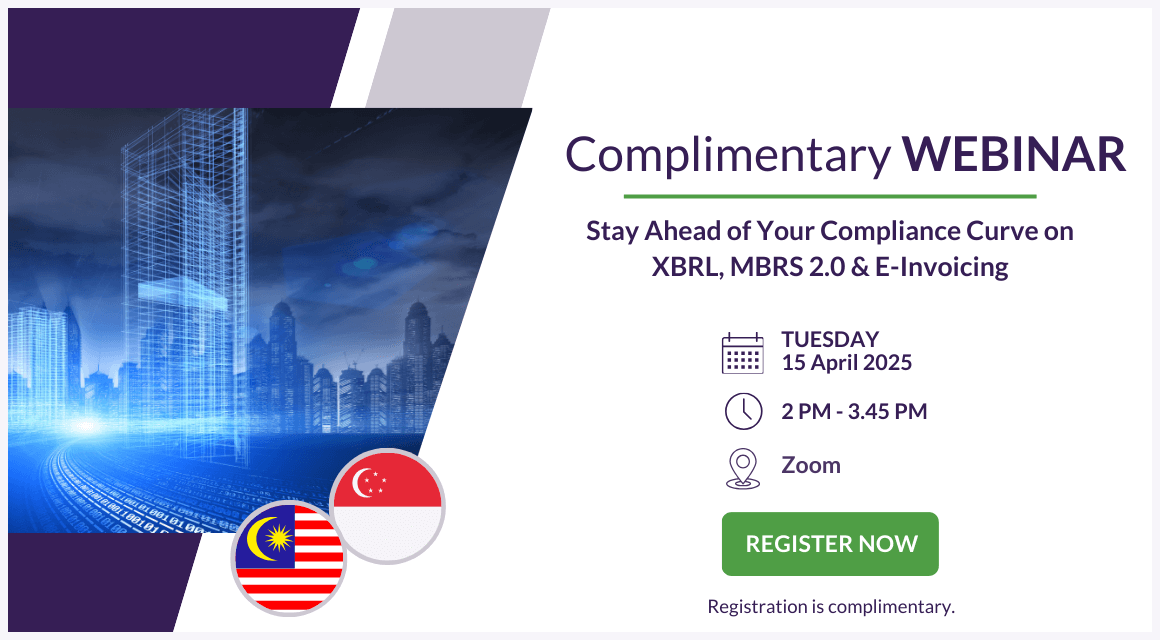

|

| |

As businesses in our region adapt to the evolving landscape of financial reporting, it’s essential to stay informed about key regulatory developments that enhance transparency and streamline processes.

In Singapore, the Accounting and Corporate Regulatory Authority (ACRA) requires all incorporated companies to submit their financial reporting in eXtensible Business Reporting Language (XBRL). This requirement not only ensures that submissions are structured and machine-readable but also significantly improves data transparency and analysis. Companies must choose from one of four formats —Full XBRL, Simplified XBRL, XBRL FSH for Banks, or XBRL FSH for Insurers. While essential, conversion to XBRL can be complex, requiring careful handling of data to maintain accuracy in reporting.

Meanwhile, in Malaysia, the Companies Commission of Malaysia (CCM) has also implemented a similar requirement, making it mandatory for companies to submit financial statements, annual returns, and exemption applications via the Malaysian Business Reporting System (MBRS). The system employs the XBRL format, enhancing transparency and efficiency while helping companies improve data quality and reduce errors.

Notably, as of 25th September 2024, Malaysia has launched MBRS 2.0, which introduces enhanced features designed to simplify financial reporting even further. This updated system expands data classification and improves consistency, allowing companies to categorise financial information more accurately and ensuring compliance with CCM regulations.

Here’s an overview of Singapore’s XBRL and Malaysia’s MBRS standards:

|

|

|

| |

| XBRL (Singapore) | MBRS (Malaysia) | Regulatory Body | ACRA | CCM | Introductory Date | 2007 (mandatory for filing financial statements) | 2018 (introduced as part of CCM’s digital transformation) | Updates in Recent Versions | Enhanced taxonomy, new data points for compliance | MBRS 2.0 enhances taxonomy and compliance features | Coverage | Mandatory for most Singapore-incorporated companies | Mandatory for certain company filings with SSM (primarily to private limited companies [Sdn. Bhd.]) | Scope of Filing | Includes financial statements such as balance sheets, profit and loss accounts in structured XBRL taxonomy | MBRS 2.0 expands beyond financial statements to include compliance reports, non-financial disclosures, and governance-related information. | Filing Platform | BizFinX portal for submission | MBRS portal for online submission |

|

|

|

| |

Adapting to the requirements of both Singapore’s XBRL and Malaysia’s MBRS can present several challenges. We take a look at 6 common issues companies may face: |

|

|

| |

| 1. Data Mapping ComplexityFinancial data must be accurately mapped to each system's taxonomy, especially for companies with complex structures. |

|

|---|

| | 2. Multi-Entity ReportingConsolidating data for multiple entities can be complex, as each has its own formats thus increasing the risk of errors. |

|

|---|

|

|

|

| |

| 3. Need for Technical ExpertiseXBRL and MBRS require specialised knowledge, and a lack of in-house expertise can lead to delays and compliance risks. |

|

|---|

| | 4. Frequent Taxonomy UpdatesRegular updates, like MBRS 2.0, require ongoing attention to ensure data stays properly formatted. |

|

|---|

|

|

|

| |

| 5. Software ChallengesSelecting the right conversion software is critical, as the wrong choice can lead to inefficiencies or errors. |

|

|---|

| | 6. Accuracy RequirementsAccurate data is vital. Errors in conversion can lead to non-compliance and costly re-submissions. |

|

|---|

|

|

|

| |

As these developments unfold, it’s clear that both Singapore and Malaysia are prioritising better data management and reporting standards, ultimately fostering a more transparent and efficient business environment. Staying ahead of these changes will be crucial for companies looking to navigate the complexities of financial reporting successfully. |

|

|

| |

|

| |

With these complexities in mind, outsourcing XBRL and MBRS conversion to a corporate service provider like BoardRoom can greatly enhance efficiency and streamline processes.

Here are some key advantages when companies choose to outsource their XBRL/MBRS conversion and filing process:

- Expertise, Scalability, & Compliance

Leverage expert insights to minimise errors and ensure compliance, while easily adapting services to meet evolving reporting needs and regulations.

- Cost & Time Savings

Lower your expenses and avoid fines associated with filing errors, as well as costs for specialised software and training, by ultilising high-quality services where providers handle the end-to-end conversion process on your behalf.

- Streamlined Processes & Quality Control

Accelerate financial reporting and ensure timely submissions, backed by rigorous quality control measures that enhance accuracy and minimise costly corrections.

Ready to outsource your company’s XBRL and MBRS conversion?

BoardRoom is here to help improve efficiency, reduce costs, and minimise compliance risks.

Let our team of experts assist you in enhancing your reporting accuracy and paving the way for your business success.

|

|

|

|

| |

|

|

|

| |

|

|

|

| |

Copyright © 2024 Boardroom Pte Ltd.

All rights reserved. |

| |

|---|

| | |

|

|